Establishing an Emergency Fund: Why This Is the Most Important Step When Managing Money

Emergency Fund- Unexpected expenses are a part of life. Whether it’s a sudden medical bill, job loss, or urgent home repair, financial surprises can disrupt even the most carefully planned budget. That’s why building an emergency fund is considered the foundation of smart personal finance.

In this guide, you’ll learn what an emergency fund is, why it matters, how much you should save, and practical strategies to build and manage it effectively.

What Is an Emergency Fund?

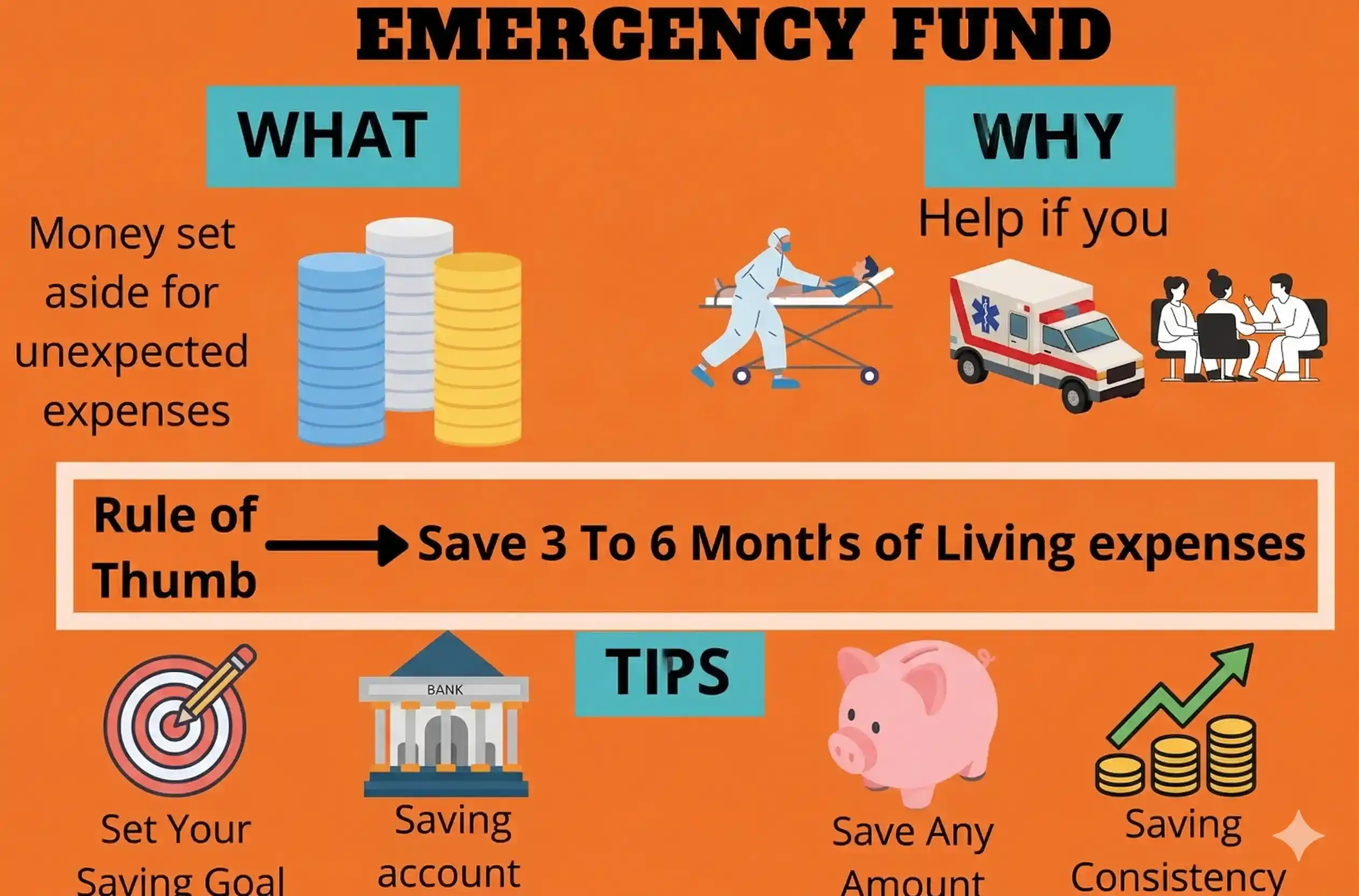

An emergency fund—also known as a rainy-day fund—is money set aside specifically to cover unexpected and essential expenses. These may include:

- Medical emergencies

- Job loss

- Urgent home repairs

- Car breakdowns

Unlike regular savings, this fund is strictly reserved for real emergencies—not for shopping, travel, or lifestyle upgrades.

The biggest advantage? It helps you avoid relying on credit cards, loans, or debt during financial crises.

Why Is an Emergency Fund So Important?

Financial expert Christine Luken once shared that before she had an emergency fund, every unexpected expense created two problems: the emergency itself and the financial stress that followed.

That’s the reality for many people.

An emergency fund acts like a financial shock absorber, protecting you from falling into debt and giving you peace of mind when life becomes unpredictable.

Here are four key situations where an emergency fund becomes essential:

1. Job Loss

Losing your primary source of income can be devastating. With an emergency fund, you can still cover essential expenses like:

- Rent

- Utilities

- Food

More importantly, it gives you time to find the right job, instead of rushing into a poor career decision out of financial pressure.

2. Medical and Dental Expenses

Even with insurance, healthcare costs can be unpredictable. Deductibles, uncovered treatments, or emergencies can quickly become expensive.

An emergency fund allows you to focus on recovery instead of financial stress, which is crucial during difficult times.

3. Home Repairs

From plumbing issues to broken appliances, home repairs often happen without warning.

Without savings, you might rely on credit cards or delay repairs—both of which can cost more in the long run.

With an emergency fund, you can handle these issues immediately and efficiently.

4. Car Repairs

For many people, a car is essential for daily life and work.

Unexpected repairs like brake replacements or engine issues can cost hundreds—or even thousands—of dollars. An emergency fund ensures you can fix your vehicle quickly without financial strain.

When Should You Use Your Emergency Fund?

A simple rule:

👉 Use your emergency fund only for essential and urgent expenses.

Appropriate situations include:

- Losing your job

- Medical emergencies

- Necessary home or car repairs

- Essential living costs when income drops

Avoid using it for:

- Shopping or entertainment

- Subscriptions or luxury services

- Non-essential upgrades

If your checking account can’t cover basic living expenses, then it’s time to use your emergency fund.

Where Should You Keep Your Emergency Fund?

Your emergency fund should be:

- Easily accessible

- Safe from market risk

- Separate from daily spending accounts

Best options include:

- High-yield savings accounts

- Money market accounts

- Short-term deposits (CDs)

Avoid investing this money in stocks or long-term assets, as you may need it quickly.

How Much Should You Save?

A common recommendation is to save:

👉 3 to 6 months of living expenses

👉 Ideally up to 12 months for extra security

Example:

If your monthly expenses are $1,000 →

- Minimum fund: $3,000

- Ideal fund: $6,000 – $12,000

To calculate your goal:

Monthly expenses × Number of months = Emergency fund target

How to Build an Emergency Fund

Building an emergency fund may seem overwhelming, but it becomes manageable with the right approach:

1. Start Small

Begin with a realistic goal like $500–$1,000.

2. Save Consistently

Set aside a fixed amount each month, even if it’s small.

3. Cut Unnecessary Expenses

Reduce spending on non-essentials like subscriptions or dining out.

4. Increase Your Income

Consider side hustles such as:

- Freelancing

- Online work

- Delivery or part-time jobs

Consistency matters more than speed.

How to Manage Your Emergency Fund

Once you’ve built your fund, maintaining it is just as important:

- Use it only when necessary

- Rebuild it immediately after use

- Adjust your budget during emergencies

- Avoid touching long-term investments

Think of your investments as long-term assets and your emergency fund as short-term protection.

Rebuilding After Using Your Fund

If you need to use your emergency savings, don’t panic—that’s exactly what it’s for.

To rebuild it:

- Reassess your budget

- Cut temporary expenses

- Increase savings contributions

- Use extra income sources

Even saving a small amount monthly can help you recover over time.

Final Thoughts

An emergency fund is not just a financial tool—it’s a form of financial security and peace of mind.

Life is unpredictable, but your finances don’t have to be. By building and maintaining an emergency fund, you protect yourself from debt, reduce stress, and gain the freedom to handle life’s challenges with confidence.