Is the 50/30/20 Rule Really Suitable for Students and Working Professionals?

Managing personal finances can feel overwhelming—especially when you’re juggling tuition fees, rent, or the rising cost of living. That’s why simple budgeting frameworks like the 50/30/20 rule have gained massive popularity.

But is this rule truly effective for everyone, particularly students and working professionals? Or does it need adjustments to fit real-life financial situations?

In this guide, we’ll break down how the 50/30/20 rule works, its benefits, and how you can adapt it to suit your income and lifestyle.

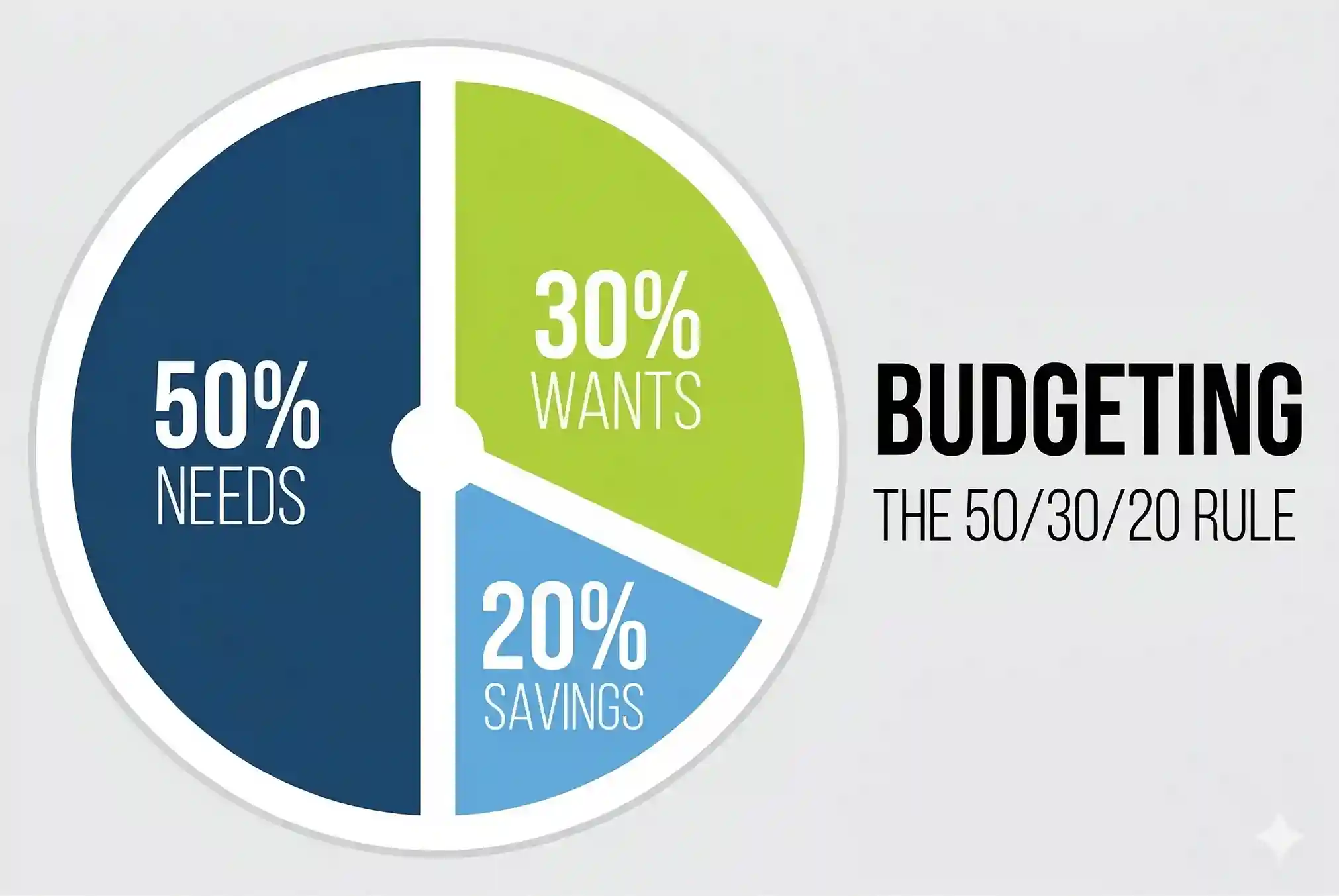

What Is the 50/30/20 Rule?

The 50/30/20 rule is a straightforward budgeting method that divides your monthly net income into three categories:

- 50% for essential needs

- 30% for wants (lifestyle expenses)

- 20% for savings and financial goals

Example:

If you earn $2,000 per month:

- $1,000 → Needs

- $600 → Wants

- $400 → Savings

This approach creates a balance between living in the present and preparing for the future.

Originally popularized by economist and U.S. senator Elizabeth Warren, this rule has become a global reference point for beginner-friendly financial planning.

Why Is Saving Important?

Saving is the foundation of financial stability. It helps you:

- Handle unexpected expenses (emergencies, medical bills)

- Plan long-term goals (education, business, investments)

- Reduce financial stress and uncertainty

A structured method like the 50/30/20 rule ensures that saving becomes a priority—not just an afterthought.

How the 50/30/20 Rule Works

1. 50% for Essential Needs

This category includes unavoidable expenses necessary for daily living:

- Rent or mortgage

- Utilities (electricity, water, internet)

- Groceries

- Transportation

- Insurance and minimum debt payments

💡 Tip: If your needs exceed 50%, consider optimizing your expenses by cutting unnecessary costs or finding more affordable alternatives.

2. 30% for Wants

This portion is for non-essential spending that improves your quality of life:

- Entertainment and hobbies

- Dining out

- Travel

- Subscriptions (Netflix, Spotify, etc.)

- Shopping

This category allows you to enjoy your money—without guilt—as long as you stay within limits.

3. 20% for Savings and Financial Goals

This is the most important part for long-term financial health:

- Emergency fund

- Investments

- Education savings

- Debt repayment

💡 Pro Tip: Transfer your savings into a separate account to avoid accidental spending.

Step-by-Step Guide to Applying the 50/30/20 Rule

- Calculate your net monthly income (after taxes)

- Divide it using the 50/30/20 percentages

- Track and categorize your expenses

- Adjust gradually—don’t make drastic changes overnight

- Review monthly to stay on track

Consistency is key to making this method work effectively.

Benefits of the 50/30/20 Rule

✔️ Simple and Easy to Follow

No complicated spreadsheets or financial expertise required.

✔️ Promotes Financial Discipline

Saving becomes a fixed habit instead of an optional action.

✔️ Creates Balance

You can enjoy your income while still preparing for the future.

✔️ Increases Spending Awareness

Helps identify unnecessary expenses and improve decision-making.

Is the 50/30/20 Rule Suitable for Students?

Yes—but with adjustments.

Students often have limited or irregular income, so a strict 20% savings rate may not be realistic.

Suggested approach:

- Focus on building the habit of saving, even if it’s just 5–10%

- Reduce “wants” spending first

- Use student discounts and budgeting apps

👉 The goal is not perfection—it’s consistency.

Is It Suitable for Working Professionals?

For full-time workers, the rule is more applicable—but still flexible.

Challenges:

- High rent or living costs may exceed 50%

- Debt (student loans, credit cards) can impact savings

Solution:

- Adjust ratios (e.g., 60/20/20 or 50/20/30)

- Increase savings gradually as income grows

How to Adapt the Rule to Your Situation

The 50/30/20 rule is not a strict formula—it’s a guideline.

You can modify it based on your financial reality:

- Low income: Start with smaller savings (even 5%)

- Freelancers/self-employed: Adjust monthly due to income fluctuations

- Low expenses: Increase savings to 30% or more

👉 Flexibility is what makes this rule sustainable.

Combine the 50/30/20 Rule with Other Strategies

To maximize results, you can combine it with:

- 52-week savings challenge (gradual saving habit)

- Pareto Principle (80/20 rule) to cut major expenses

- Emergency fund planning for financial security

These methods can strengthen your overall financial strategy.

Frequently Asked Questions (FAQs)

Does the 50/30/20 rule work with low income?

Yes. Start small and increase your savings rate over time.

Can freelancers use this method?

Absolutely. Just calculate your average monthly income and review your budget more frequently.

What if I can’t save 20%?

That’s okay. Save what you can—the habit matters more than the percentage.

Is this better than other budgeting methods?

It depends. The 50/30/20 rule is ideal for simplicity, while other methods may offer more detailed control.

Conclusion

The 50/30/20 rule is a powerful yet simple framework for managing your money. It helps you balance essential expenses, personal enjoyment, and long-term financial goals.

However, it’s not a one-size-fits-all solution.

Whether you’re a student or a working professional, the key is to adapt the rule to your reality, stay consistent, and continuously improve your financial habits.

👉 Start small, stay disciplined, and your financial future will thank you.