Understanding Personal Cash Flow Correctly: Earn – Spend – Save – Grow

In today’s rising cost-of-living environment, many people find themselves asking a familiar question: “Where did all my money go?” If this sounds like you, the issue may not be how much you earn—but how well you manage your personal cash flow.

Mastering your cash flow is the foundation of financial stability. When you clearly understand how money flows in and out of your life, you gain control, reduce stress, and unlock opportunities to save, invest, and grow your wealth.

Key Takeaways

- A personal cash flow strategy helps you track income and expenses effectively

- Knowing your net worth gives clarity about your financial position

- A cash flow statement reveals why money runs out (or doesn’t) each month

- You can improve cash flow by cutting costs, reducing debt, and increasing income

- Positive cash flow creates flexibility to achieve long-term financial goals

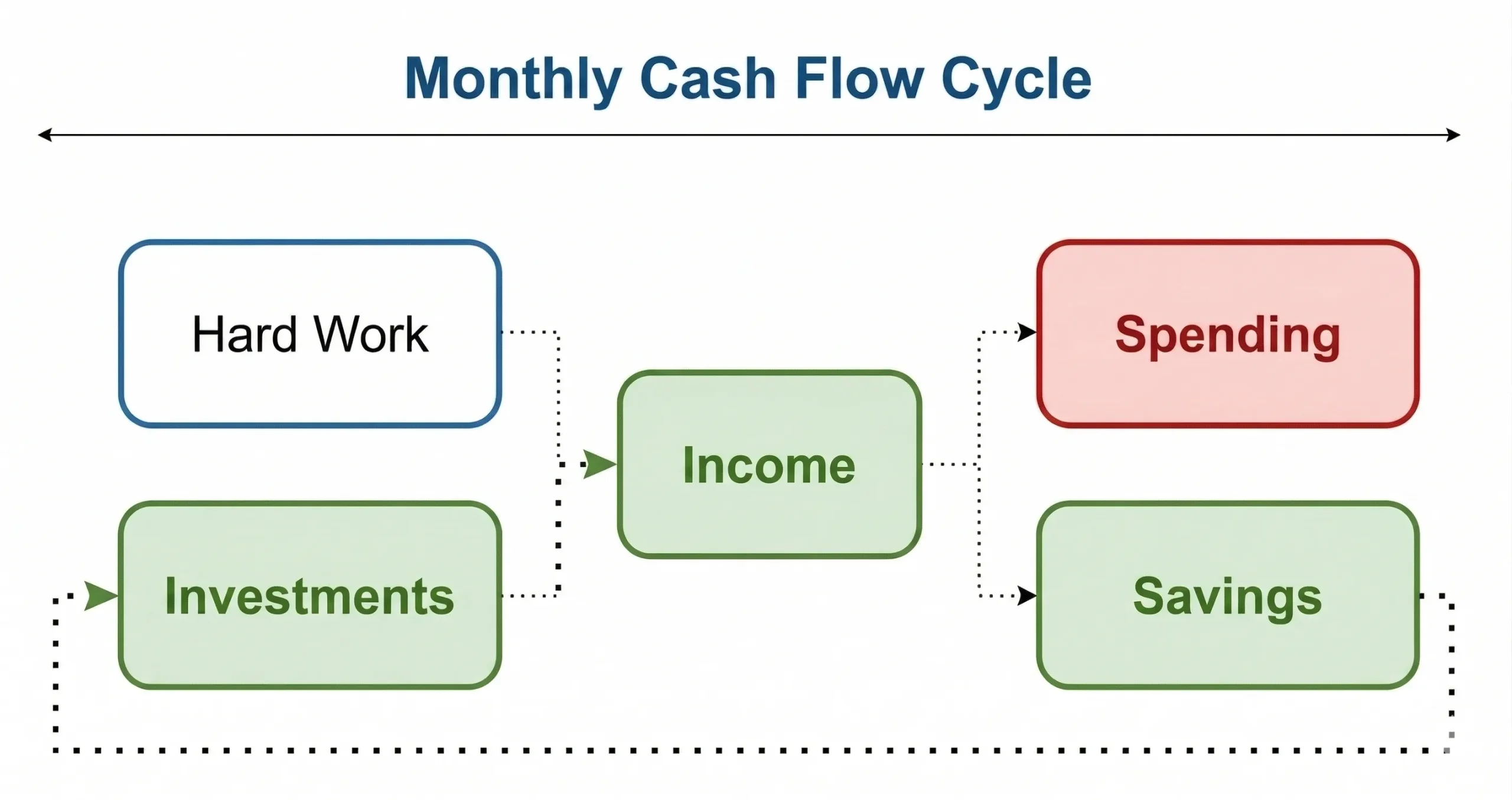

What Is Personal Cash Flow?

Personal cash flow refers to the movement of money in your life—how much you earn (inflows) versus how much you spend (outflows).

A strong cash flow strategy ensures that:

- Your income covers essential expenses

- You can save for emergencies

- You still have room to invest and grow your money

Think of it as a simple cycle:

=> Earn → Spend → Save → Grow

Why Understanding Cash Flow Matters

Without tracking your finances, it’s easy to:

- Overspend without realizing it

- Accumulate debt

- Miss opportunities to save or invest

On the other hand, managing your cash flow helps you:

- Stay financially organized

- Make smarter decisions

- Build long-term wealth

Step 1: Calculate Your Net Worth

Before diving into cash flow, you need to understand your financial position.

Net worth = Total assets – Total liabilities

- Assets: Savings, investments, property

- Liabilities: Loans, credit cards, debts

=> If your assets exceed liabilities → Positive net worth

=> If liabilities are higher → Negative net worth

Knowing this number helps you set realistic financial goals.

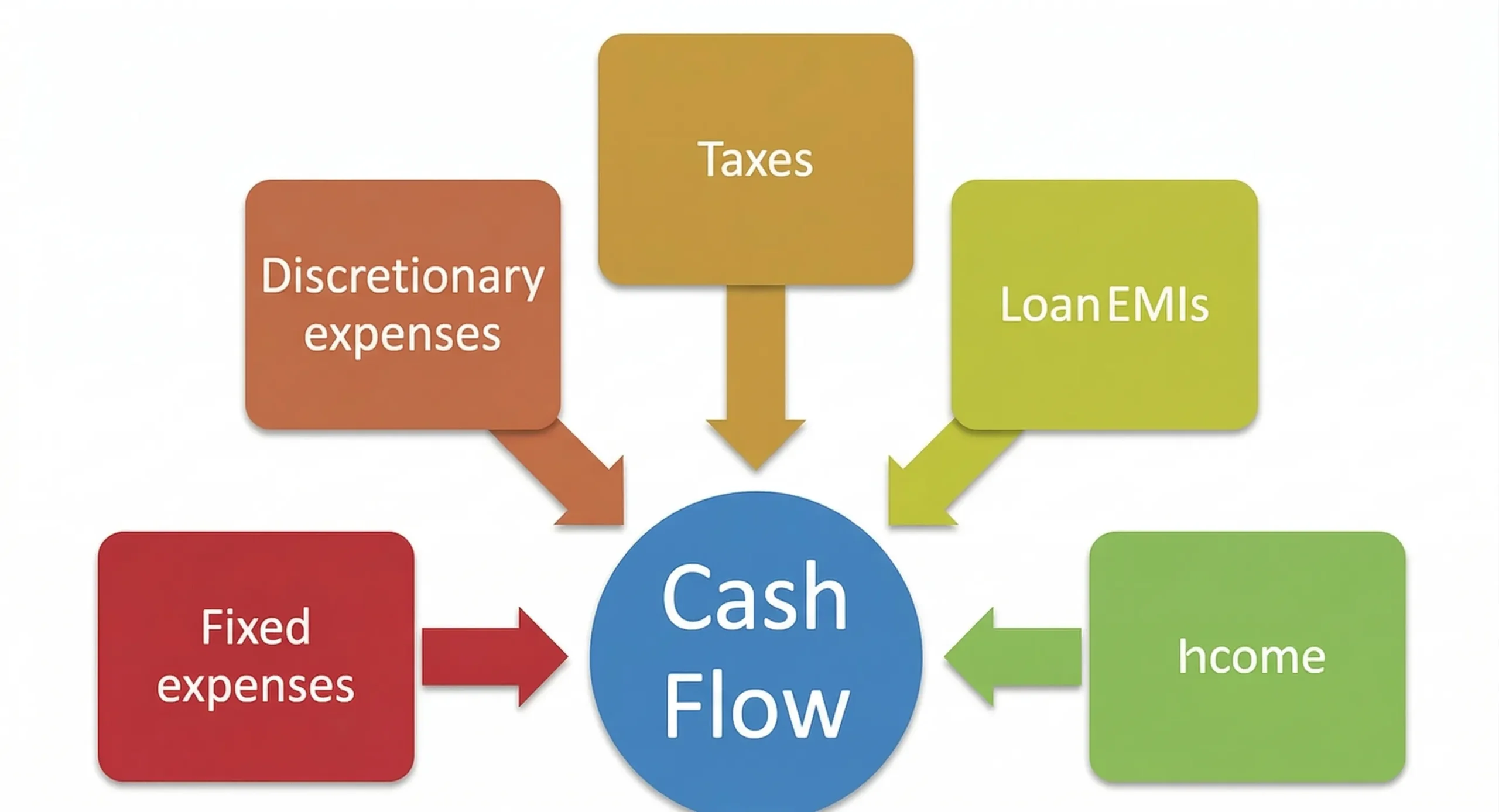

Step 2: Build a Personal Cash Flow Statement

A cash flow statement shows exactly how money moves in your life.

1. Track Your Income (Inflows)

Include:

- Salary (after tax)

- Side hustles

- Bonuses or benefits

- Passive income

2. Track Your Expenses (Outflows)

Divide them into:

Essential expenses

- Rent or mortgage

- Utilities

- Food

- Transportation

Non-essential expenses

- Entertainment

- Dining out

- Subscriptions

- Travel

Don’t forget:

- Debt payments

- Savings contributions (yes, they count as outflows too!)

Step 3: Calculate Net Cash Flow

Here’s the key formula:

Net Cash Flow = Total Income – Total Expenses

What it means:

- Positive cash flow → You earn more than you spend ✅

- Negative cash flow → You spend more than you earn ❌

Positive cash flow gives you the power to invest, save, and grow wealth.

Step 4: Analyze Your Spending Habits

Track your finances over at least 3 months to identify patterns:

- Where are you overspending?

- Which expenses can be reduced?

- Are you saving enough?

This step is where real financial awareness begins.

How to Improve Your Cash Flow

1. Cut Unnecessary Expenses

Small costs add up quickly:

- Unused subscriptions

- Impulse purchases

- Lifestyle inflation

=> Review your spending and eliminate what doesn’t add value.

2. Automate Your Savings

Set up automatic transfers to:

- Savings accounts

- Emergency funds

This ensures you save first, not last.

3. Use Credit Cards Strategically

If used wisely, credit cards can:

- Provide cashback

- Earn reward points

⚠️ But always avoid carrying high-interest balances.

4. Apply the 50-30-20 Rule

A simple budgeting framework:

- 50% Needs (rent, food, bills)

- 30% Wants (lifestyle spending)

- 20% Savings & Debt Repayment

Adjust percentages depending on your situation.

5. Increase Your Income

Consider additional income streams:

- Freelancing or side hustles

- Rental income (real estate)

- Dividend-paying investments

💡 Passive income is key to long-term financial growth.

6. Reduce and Manage Debt

High-interest debt reduces your cash flow quickly.

Solutions:

- Consolidate debt at lower interest rates

- Focus on paying off high-interest balances first

7. Optimize Your Mortgage or Loans

If applicable:

- Refinance to lower monthly payments

- Extend repayment terms for better cash flow

8. Adjust Your Plan Over Time

Life changes—your finances should too.

Update your cash flow when:

- Income increases

- Expenses rise

- Major life events occur

Final Thoughts

Your money shouldn’t feel like a mystery.

Understanding your cash flow and net worth is the first step toward financial freedom. Once you know where your money goes, you can take control—cut waste, boost savings, and build a future that aligns with your goals.

Remember:

It’s not just about how much you earn—it’s about how well you manage, save, and grow it.